PRIMELEGAL | Streamlining IPOs: How SEBI’s Operational Fixes Will Prevent Listing Delays and Protect Investors

Abstract

The rapid growth of India’s IPO market has increased the participation of venture capitalists, private equity funds, and other pre-IPO investors. To prevent sudden large-scale selling of shares after listing and to maintain market stability, the Securities and Exchange Board of India (SEBI) has traditionally imposed lock-in requirements under the ICDR Regulations, requiring non promoter pre-IPO investors to hold their shares for six months after the IPO. Nevertheless, operational difficulties and delays emerged in the IPO process as a result of operational issues (for example, depositories could not mark pledged shares as locked in). In response, SEBI has suggested changes to the operational process(s), while retaining the same lock-in period (i.e., six months); only through a new operational process. The proposed operational changes include amending the Articles of Association; designating pledged shares as non-transferrable via depositories; maintaining lock-in requirements after invocation; and enhancing offer document disclosure. Although the operational changes are likely to enhance transparency and ease the IPO process, several risks are involved, such as the possibility of regulatory arbitrage, challenges in technology implementation, and the need for issuers to comply. For this reason, it is crucial for market stability and investor protection that there be proactive coordination between issuers, investors, and regulators, and that disclosures be robust.

Keywords

IPO Regulation, Lock in Period, Pre IPO Investors, Securities Regulation, Corporate Governance, Capital Markets, Investor Protection, Depository Mechanism, Articles of Association, Ease of Doing Business, Pledged Shares, Market Stability

Introduction

With a spike in initial public offerings and rising involvement from venture capital and private equity investors, India’s capital market has grown significantly in recent years. Regulatory protections have been crucial to maintaining market stability during this expansion. The SEBI ICDR Regulations’ lock-in requirement for pre-IPO investors is one such protection. However, the Securities and Exchange Board of India (SEBI) has proposed certain amendments to ease the procedural aspects of these norms while maintaining investor protection due to practical difficulties in implementing these lock-in provisions.

By addressing operational challenges in enforcing lock in restrictions, especially when pledged shares are involved, these proposed reforms seek to uphold the regulation’s core goals. The modifications show SEBI’s effort to strike a balance between investor protection, market stability, and ease of doing business.

Existing Lock in Norms and Their Purpose

According to Regulation 17 of the ICDR Regulations (the legislation that dictates the current regulatory framework) all pre-issue capital that non-promoter investors hold in a company must be locked-in for a period of 6 months after the issue date of a company’s IPO. By contrast, promoters are subject to a longer lock-in period. Specifically, minimum promoter contributions are required to be locked for at least 1 year from the date of the IPO allotment, whereas some preferential allotments made to promoters are subject to a lock-in exceeding 3 years from the date of the IPO allotment. The primary objective of requiring lock-in periods is to prevent early investors from cashing out immediately after IPO, thus protecting retail investors from large-scale sales that could negatively impact the market price of the newly listed company’s shares and diminish overall market confidence. Without lock-in provisions, investors such as venture capitalists and private equity funds would likely take advantage of their ability to sell a substantial number of shares shortly after a company goes public, which would significantly increase the supply of available shares in the market and cause the stock price to drop dramatically.

Thus, lock in norms fulfil a number of crucial purposes. They first aid in maintaining price stability throughout the post listing phase. Secondly, they align early investors’ interests with the company’s long term growth. Third, they deter speculative investments in pre IPO placements that are only intended to yield immediate profits. As a result, these regulations are crucial to preserving stability and confidence in India’s capital markets.

Operational Challenges Under the Current System

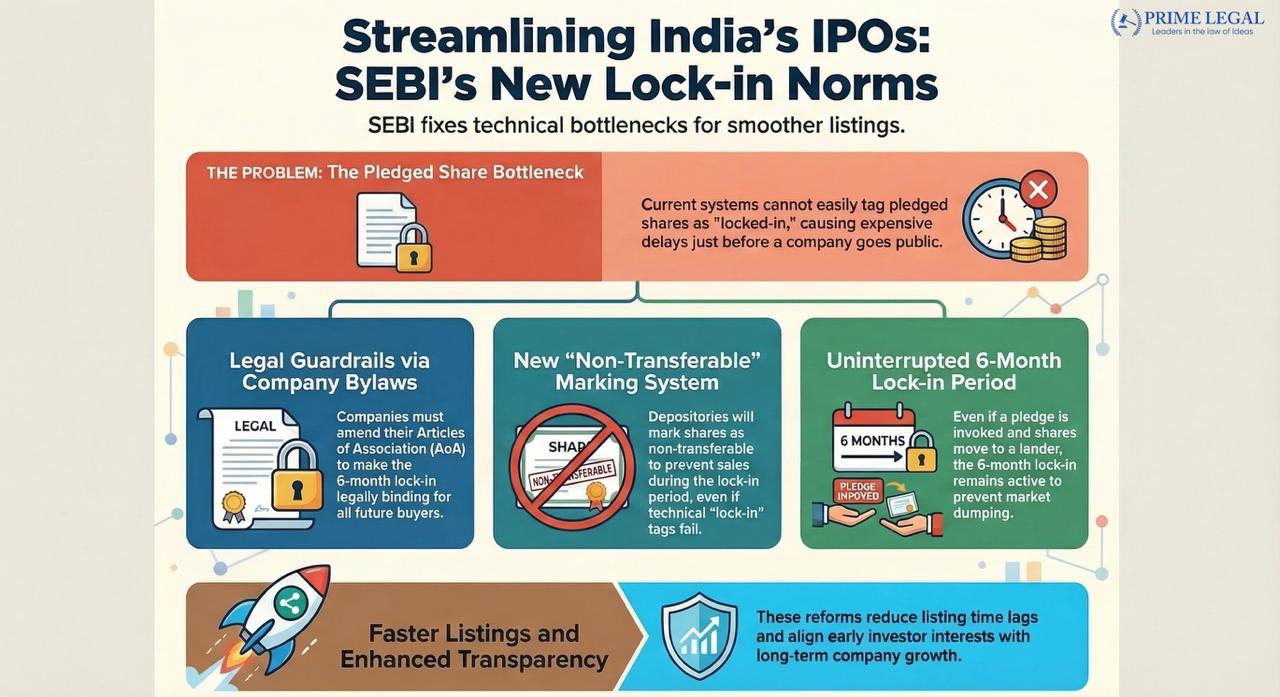

Even though the lock in rules have strong policy goals, putting them into practice has been hard. One of the biggest problems is that depositories can’t tag pledged shares with lock in restrictions.

A lot of the time, investors who buy shares before an IPO put them up as collateral for loans with banks. Depositories can’t easily mark pledged shares as locked in, though, because of the way things are set up now. So, these shares are still technically transferable until the pledge is used. In this way, lock in norms serve many important purposes.

They first aid in maintaining price stability throughout the post listing phase. Secondly, they align early investors’ interests with the company’s long term growth. Third, they deter speculative investments in pre IPO placements that are only intended to yield immediate profits. As a result, these regulations are crucial to preserving stability and confidence in India’s capital markets.

Also, shareholders can make or break pledges just before the IPO filing, which makes it hard for companies to keep track of how many shares they own. Issuers have often said that it is hard to find shareholders who have pledged shares, and in some cases, they have even had trouble getting in touch with certain investors or have not been able to get them to cooperate.

These problems lead to what is known as a “last mile compliance problem.” Even if a company has met most of the rules for its IPO, the listing process may be delayed if it finds pledged shares that can’t be properly locked in. Companies then have to take quick steps to fix the problem, like asking for individual waivers or changing the way their shares are held. These kinds of delays can be expensive and mess up carefully planned IPO schedules.

SEBI has suggested changes to the lock in rules that will make them easier to enforce without losing sight of their main goal.

SEBI’s Proposed Amendments

In a consultation paper released in November 2025, SEBI suggested a number of technical changes to make it easier to enforce pre-IPO lock-in requirements.

The main point of the proposals is not to shorten the lock in period, but to change how the lock in is put into place and monitored.

One of the most important proposals is the requirement that companies amend their Articles of Association (AoA) before filing for an IPO. These changes would make it clear that pledged pre IPO shares will still be subject to the six month lock in period. Adding the lock in requirement directly to the company’s constitutional documents makes it legally binding on everyone who buys those shares in the future.

Another important suggestion is that lock in should stay in place even after the pledge is invoked. If a pledged share is given to a lender after the pledge is invoked, the share will stay locked in for the rest of the six month period. This makes sure that pledge agreements can’t get around the lock in restriction.

SEBI has also suggested adding a “non transferable” marking system to the depository system. If the system can’t technically tag shares as locked in, the depository will instead mark them as non transferable. This stops the shares from being transferred during the lock in period.

Rationale Behind the Proposed Reforms

SEBI’s suggestions show that they are trying to strike a balance between two important goals of regulation: protecting investors and making it easier to do business.

Lock in rules are needed to keep the market honest and stop people from acting in a speculative way. However, procedures that are too strict can make things harder for businesses and slow down IPOs. This can make companies less likely to go public. SEBI wants to get rid of operational bottlenecks while keeping the same level of investor protection by adding things like non-transferable marking and AoA amendments.

Potential Implications

If the SEBI proposals are implemented efficiently, the efficiency of the Indian IPO market is likely to improve considerably.

One of the major benefits of the SEBI proposals is the reduced time lag in the listing of shares. The technical issues faced in the listing of shares due to pledged shares will be resolved. The companies will be able to implement their listing plans without any issues.

The second major benefit of the SEBI proposals is the increased transparency and corporate governance standards. The changes to the AoA and the disclosures in the offer documents ensure that all the stakeholders are aware of the lock in issues.

The third major benefit of the SEBI proposals is the increased confidence of investors. The new regulations will ensure that investors are not subjected to any sudden share dumping.

However, the reforms also introduce additional responsibilities for companies. Issuers must carefully plan AoA amendments, obtain shareholder approvals, and coordinate with depositories and lenders. Failure to comply with these requirements could lead to regulatory penalties or legal disputes.

Conclusion

The goal of SEBI in introducing measures such as the amendments to Articles of Association (AoA) and the marking of non-transferable shares and increasing the level of disclosure is to streamline the IPO compliance process, while preserving the integrity of the market and protecting investors. This reform represents an important step in the ongoing evolution of the relationship between corporate governance, securities regulation and market efficiency in the context of Company Law. It demonstrates that regulatory frameworks will continue to evolve to reflect changes in market conduct, while at the same time fulfilling their fundamental objective of providing investor protection.

If these proposals are successfully implemented, the changes could enhance India’s capital market efficiency, allow for a smoother transition to listing on an exchange for new issuers, as well as improve the level of commitment from initial investors in newly-listed companies to support the long-term success of the company.

“PRIME LEGAL is a National Award-winning law firm with over two decades of experience across diverse legal sectors. We are dedicated to setting the standard for legal excellence in civil, criminal, and family law.”

WRITTEN BY: KISLAY RAJ