CASE NAME: Bhagyalaxmi Co-Operative Bank Ltd. Versus Babaldas Amtharam Patel (D) Through Legal Representatives & Others

CASE NO.: Civil Appeal No. 3200 of 2016

COURT: Supreme Court of India

DATE: 27-02-2026

QUORUM: THE HONOURABLE MRS. JUSTICE B.V. NAGARATHNA & THE HONOURABLE MR. JUSTICE UJJAL BHUYAN

FACTS

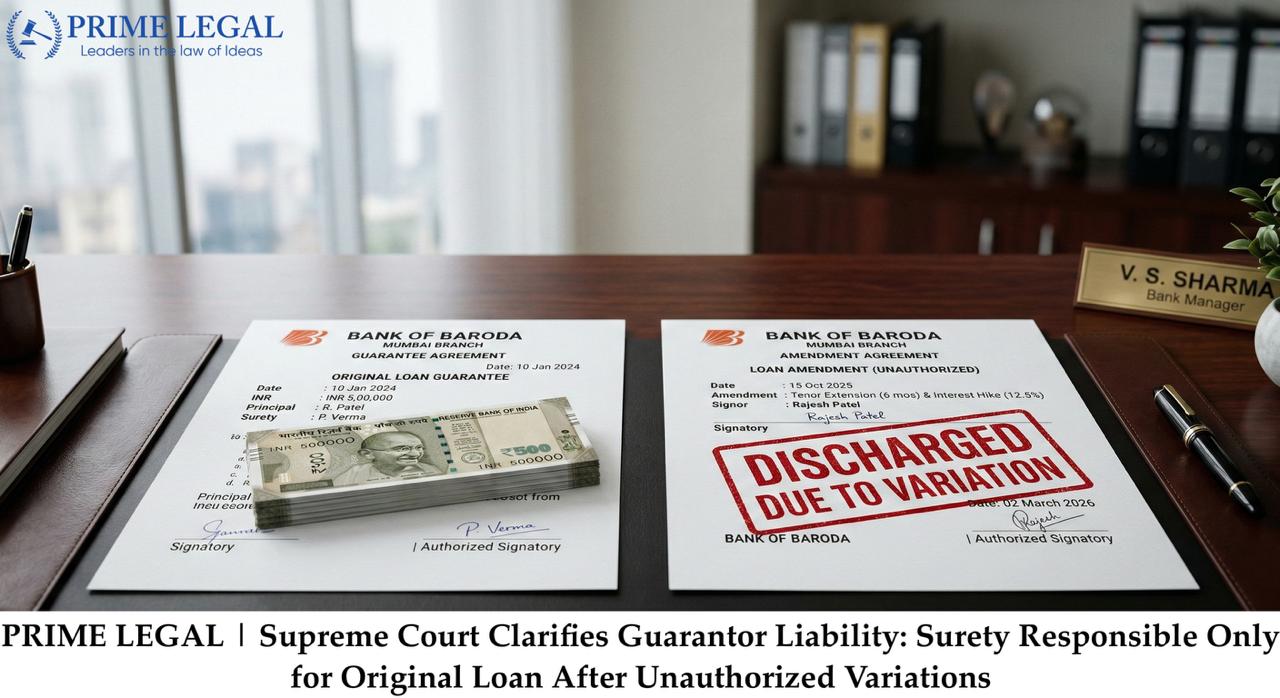

On 30 October 1993, Respondent No. 6 {M/s Darshak Trading Company} took a loan of Rs. 4,00,000 from Bhagyalaxmi Co-Operative Bank Ltd. Respondent No. 1 & 2 became the sureties for the loan being sanctioned by the bank. Here an excess withdrawal took place which the bank approved without the consent of the sureties. The respondent no. 6 has hypothecated his mercantile goods to the creditor. The respondent hereby fails to repay the loan amount and the bank sues the sureties for the repayment of the actual loan amount including interest that is Rs.26,95,196.75.

The sureties have not been made aware of the amount of loan being taken by the respondent no. 6 but were held liable for the payment of the full loan amount to the bank. By judgment dated 09.07.2001, the Board of Nominees decreed the suit and accepted the claim of the appellant only as regards respondent No.6 who was the principal borrower to the extent of the Rs.26,95.196.75 to be the sole bearer of the loan.

ISSUES

- Whether the sureties are liable for the loan when the borrower withdrew amounts beyond the sanctioned limit.

- Whether allowing excess withdrawals amounts to a variance of contract under Section 133.

- Whether the sureties are discharged entirely under Section 139.

- Whether sureties can be held liable only to the extent of the original guarantee.

- Whether the creditor must first proceed against the principal debtor.

LEGAL PROVISIONS:

- Section 126 of the Indian Contract Act 1872 that defines the contract of guarantee.

- Section 128 of the Indian Contract Act, 1872 which talks about the liability of the surety.

- Section 133 of the Indian Contract Act 1872 which deals with the discharge of the surety by the variance in terms of the contract.

- Section 139 of the Indian Contract Act 1872 that deals with the act or omission of the creditor impairing the surety’s remedy.

ARGUMENTS:

APPELLANT:

Learned senior counsel Sri Raghavendra S. Srivatsa appearing for the appellant submitted that the High Court was not right in holding that under Section 133 of the Act, the sureties are liable for the entire amount or none at all. He drew our attention to Section 133 of the Act, which states that any variance, made without the surety’s consent, in the terms of the contract between the principal debtor and the creditor, discharges the surety as to transactions subsequent to the variance. Learned senior counsel further submitted that having regard to the facts of the present case, the Bank being the creditor is entitled to recover the outstanding dues from the sureties till the time when the variation in the contract occurred. However, for the subsequent dues pursuant to the variation of the contract, which was without the consent of the sureties, the sureties may not be liable.

RESPONDENTS :

The counsel of the sureties relied on the section 139 of the Indian Contract Act 1872 which states that the sureties will stand discharge from the liability because of the act of the creditor which has impaired sureties’ right to remedy. Here the bank allowed the excess with-drawl of the loan to the respondent no. 6 beyond the specified limit of Rs.4,00,000 without the consent of the sureties or without them knowing. The counsel argued that the sureties under section 139 of the Indian Contract Act 1872 hereby stand wholly discharged from the liability as their consent was not obtained for the excess with-drawl of the loan from the bank. It was stated that this act was inconsistent with the rights of the sureties. If the sureties had known about the excess with-drawl they would have protected themselves from the excess burden. But they were not being made aware of the excess amount by the creditor which has impaired their right as a surety. The counsel argued that the surety should stand completely discharged from the liabilities because of the variance. The Counsel disregarded the concept of partial liability because of the variances in the contractual terms.

ANALYSIS :

Section 133 of the Indian Contract Act 1872 grants the surety the relief to stay out of the liability as a surety when the terms of the contract are being changed without their consent. And under Section 139 of the act also makes the surety stand out of the liability when the act of the creditor has impaired the remedy available to the surety.

The SC relied on the following precedents:

- a) Radha Kanta Pal vs. United Bank of India Ltd., AIR 1955 Cal 217; which stated that the mere absence of the notice to the surety doesn’t discharge the surety from the liability as it can only be discharged when the creditor’s act has impaired the sureties’ rights. Here the surety still had remedy and henceforth stated that the mere absence of the notice doesn’t impair the remedies of the surety. Surety is discharged only if the right to remedy is prejudiced.

- b) Bishwanath Agarwala vs. State Bank of India, AIR 2005 Jhar 69; in this case it was held that the withdrawal of the loan amount will not make the surety liable for the excess with-drawl of the loan without their consent. The sureties will only be liable for the agreed amount mentioned in the original terms of the contract.

- c) State Bank of India vs. M/s Indexport Registered, (1992) 3 SCC 159; the court held that the sureties are co-extensively liable with that of the principal debtor. And the creditor can sue the sureties directly.

- d) Syndicate Bank vs. Channaveerappa Beleri, (2006) 11 SCC 506; the Supreme Court in this case held that the liability of the surety is based to the extent mentioned in the terms of the contract. If the contractual terms are based on the continuing guarantee then the sureties liability will vary in the future based on the contract terms.

It was being analyzed from these sections and judgments that the surety has certain rights available to them for the discontinuation of the contract terms and the liability.

JUDGEMENT:

The Supreme Court hereby examined the sections of the act and it was being held that only the section 133 of the Indian Contract Act 1872 will be applicable and not section 139 of the act as the creditor has not impaired the rights of the surety. They can still claim the damages from the principal debtor. Hence the court gave the judgment that the surety will be partially liable as they agreed to the original conditions of the contract which was the with-drawl of Rs.4,00,000 from the bank. Hence nullifying their liability wholly would even be unfair to the actual agreed conditions of the original contract.

CONCLUSION:

Hence it was concluded that the discharge would be partial and not total to protect the agreed terms of the contract. Hence the conclusion being made is the liability of the sureties to be acceptable till their agreed terms of the original contract.

“PRIME LEGAL is a National Award-winning law firm with over two decades of experience across diverse legal sectors. We are dedicated to setting the standard for legal excellence in civil, criminal, and family law.”

WRITTEN BY: MEENAKSHI DANGI.

Click here to read the judgment.